Fed Rate Decisions and Mortgages: What Homebuyers Should Know

When people say, “The Fed raised rates or lowered rates…”. The truth is: the Federal Reserve doesn’t directly set mortgage rates, but its decisions can/could influence the environment within which mortgage rates operate.

What the Federal Funds Rate Is (in Plain English)

The federal funds rate is the interest rate banks charge each other for overnight loans of reserve money held at the Federal Reserve. Think of banks like grocery stores at closing time: some end the day with extra inventory (cash reserves), and others realize they’re short. If one store needs supplies quickly to open tomorrow, it borrows from a store with the extra supple—just for the night.

The rate negotiated in these overnight “cash swaps” contributes to the effective federal funds rate, which is essentially the average rate across those real transactions.

Who Decides the Target Rate?

The Federal Open Market Committee (FOMC) meets eight times per year to set a target range for the federal funds rate. While banks negotiate the actual overnight loans, the Fed uses an important tool to guide the rate into that target range: the Interest on Reserve Balances (IORB) rate.

Here’s the analogy: if you can earn a guaranteed return by parking your money safely, you won’t lend it out for less. Banks operate the same way. Because the Fed pays interest (IORB) on reserve balances, banks are generally unwilling to lend reserves overnight for a lower rate than what they can earn risk-free at the Fed. That’s one reason IORB is such an effective “steering wheel” for short-term rates.

Why the Fed Raises or Lowers Rates

The Fed’s mandate is to support a healthy economy while keeping inflation under control. So the FOMC watches a wide range of indicators, including:

- inflation and wage trends

- employment conditions

- consumer spending and incomes

- business investment

- global financial conditions

If inflation is too high or growth is overheating, the Fed may raise rates to cool demand. If the economy is slowing, it may lower rates to encourage borrowing and spending.

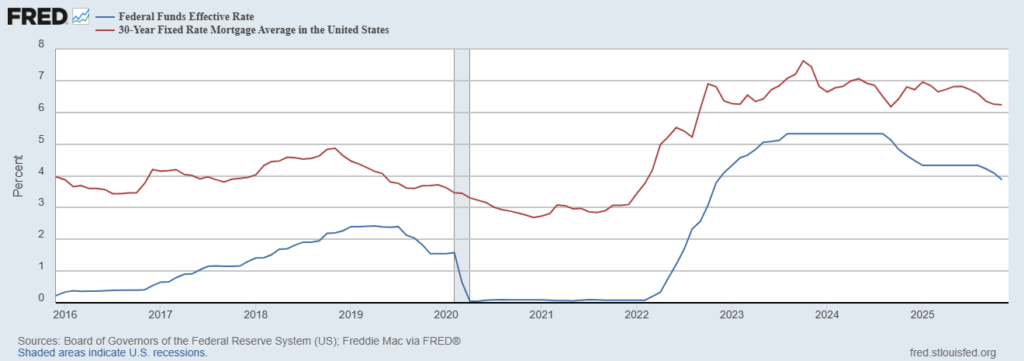

How Fed Decisions Affect Mortgage Rates

Mortgage rates are longer-term rates, shaped by things like inflation expectations, bond markets, and overall economic outlook. Even so, Fed actions can affect mortgage rates indirectly by influencing:

- expectations for future inflation

- investor demand for bonds (including mortgage-backed securities)

- the general direction of interest rates across the economy

That’s why mortgage rates can move before a Fed meeting (markets anticipate changes) or sometimes move in ways that don’t perfectly match the Fed’s exact adjustment.

What Homebuyers Can Do

You can’t control Fed policy—but you can control your strategy:

- strengthen your credit profile

- explore loan programs and term options

- consider rate-lock timing when you’re under contract

- focus on the monthly payment that fits your budget, not just the headline rate

At Family Financial Home Loans, we help homebuyers translate rate news into real decisions—so you can move forward with clarity, even when markets feel unpredictable.

Stop guessing and start planning. Mortgage rates fluctuate daily, and the best time to lock is when the time is right for you. Get a free, personalized purchase quote today to know exactly where you stand and learn the specific rate you qualify for!